Where Does Money Actually Go?

Most people remember big expenses but can't account for the rest. Learn why money feels invisible and how to develop awareness of where it actually goes.

TL;DR: How to Think Differently

- Money disappears through three channels: the obvious ones you remember, the invisible ones you forget, and the ones you're actively avoiding noticing

- "Where did it go?" is the wrong question — the better question is "What pattern am I not seeing?"

- Most people track spending after the month ends when it's already too late to understand their own behavior

- The gap between what you earn and what you have isn't always about discipline — it's often about awareness of tiny, repeated decisions

- Your money doesn't vanish mysteriously — it leaves a trail, but you're not looking at the right places

- Understanding where money goes is not the same as controlling it — this is about seeing first, judging later

Who This Is For

This is for anyone who has ever looked at their bank balance mid-month and thought, "But I just got paid."

If you earn a decent salary but feel like you're always scrambling before the next payday, this is for you. If you've ever felt guilty about not knowing where your money went, this is for you. You don't want to become the kind of person who maintains detailed spreadsheets.

This is especially for people who are tired of vague financial advice that tells them to "track expenses." It never explains why their money behaves the way it does.

You're not bad with money. You're just not paying attention to the right things yet.

Why This Invisibility Happens

Here's what usually happens:

You get your salary on the 1st. By the 5th, rent is gone. By the 10th, you've paid the maid, the phone bill, maybe cleared a credit card. By the 15th, you feel like you still have "enough." Then suddenly it's the 25th, and you're wondering what happened.

The problem isn't that you spent too much. The problem is that you don't actually know what happened between the 15th and the 25th.

Most people can tell you their rent amount. They can tell you their EMI. But ask them how much they spent on Swiggy last month. Or how much went to "small" auto rides. Or what they actually paid for that friend's birthday dinner including the cab there and back. They'll guess. Badly.

This isn't about memory. It's about attention.

We pay sharp attention to big, painful outflows. Rent hurts. EMIs hurt. School fees hurt. But we don't notice the ₹200 here, ₹500 there, ₹1,000 on a weekend. Our brain categorizes those as "nothing much."

Except when you add them up over a month, "nothing much" becomes ₹15,000.

The real issue is this: money leaves in three ways, and we only track one of them properly.

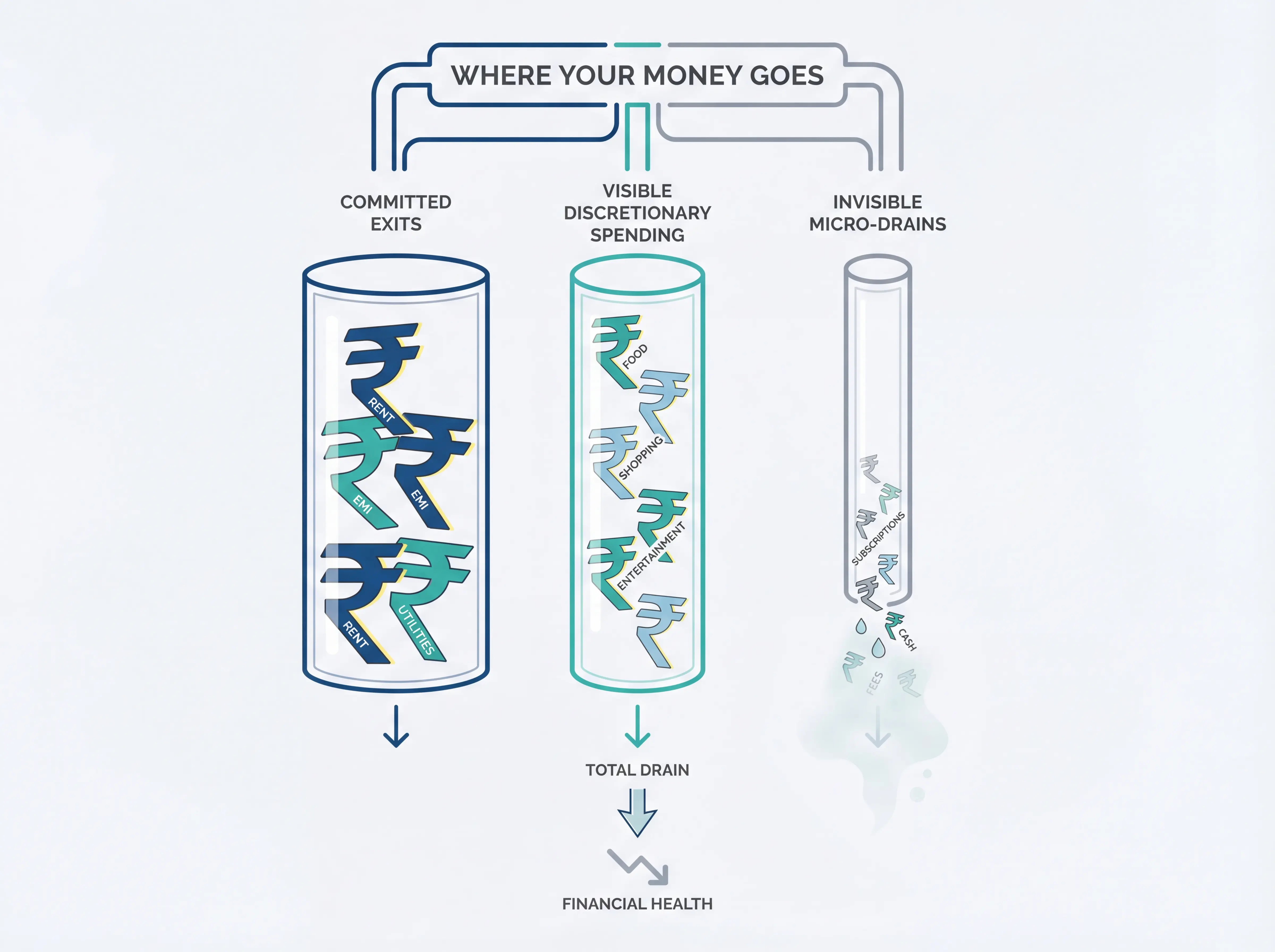

The Three Channels Your Money Actually Uses

Channel 1: The Committed Exits

These are the ones you know about. Rent. EMIs. Insurance premiums. School fees. DTH recharge. Internet bill. These are predictable, unavoidable, and usually painful enough that you remember them.

Most people think this is where their money goes. And yes, this is often the biggest chunk — maybe 40–60% of your income if you're middle-class and living in a metro.

But here's the thing: these don't explain the mystery. You know rent is ₹20,000. You know the home loan EMI is ₹18,000. These aren't the reason you're confused about your balance.

Channel 2: The Visible Discretionary Spending

This is where you think you have control. Groceries. Eating out. Shopping. Movie tickets. Fuel. Weekend trips.

You know you're spending here. You just don't know how much.

A Zomato order feels like ₹600. But when you actually check at month-end, you've ordered 12 times, and it's ₹8,000. You think you're spending ₹3,000 on groceries. It's actually ₹5,500 because you forgot the midnight Blinkit runs for milk, bread, and "just one thing."

This category feels manageable because each individual expense seems reasonable. ₹800 for groceries? Fine. ₹1,200 for dinner? It was a good restaurant. ₹450 for an auto because it was late and you were tired? Of course.

But the sum of all "reasonable" decisions is often unreasonable.

Channel 3: The Invisible Micro-Drain

This is the one people almost never see. This is where money evaporates.

Subscriptions you forgot about. Amazon Prime. Netflix. Spotify. That fitness app you used twice. The ₹150/month "premium" feature on some app you don't even open anymore.

Small cash payments you didn't note. ₹50 to the building watchman. ₹100 to the newspaper vendor. ₹200 in tips and small temple donations across the month.

The "convenience tax" you pay for not planning. Buying a ₹30 water bottle every day because you forgot your bottle at home. Paying ₹200 for parking because you were running late. Grabbing ₹150 of chips and cold drink at a petrol pump on a highway trip.

ATM withdrawals you can't account for. You took out ₹5,000 cash three weeks ago. You have ₹400 left. What happened to ₹4,600? You genuinely don't know.

This channel doesn't show up in digital transaction history. And it doesn't hurt enough to remember.

What People Get Wrong About This

"I don't spend on unnecessary things"

You probably don't. But "unnecessary" and "unnoticed" are different.

That ₹200 coffee while waiting for someone isn't unnecessary — you were thirsty, and it was hot. That ₹600 Uber instead of the metro isn't unnecessary — you were late for a meeting. That ₹1,800 grocery run on Sunday evening isn't unnecessary — you needed to cook for the week.

But when these small, necessary, reasonable decisions happen 40 times a month, they add up to ₹10,000 you didn't mentally budget for.

The mistake is thinking that "justified" means "invisible in the total."

"I'll remember the big expenses"

Yes, you will. You'll remember the ₹8,000 you spent on your niece's birthday gift. You'll remember the ₹12,000 you spent on that weekend trip to Lonavala.

What you won't remember is the ₹15,000 that left through 50 different transactions of ₹300 each. Your brain isn't wired to aggregate. It remembers peaks and valleys, not patterns.

Big expenses are easy to see. Patterns are invisible until you force yourself to look.

"If I just earned more, this wouldn't be a problem"

Here's the uncomfortable truth: people earning ₹50,000 a month say, "Once I'm at ₹1 lakh, I'll be comfortable." People earning ₹1 lakh say, "Once I'm at ₹2 lakh, I'll have surplus."

But when income doubles, expenses quietly expand to fill the gap. The Swiggy orders get more frequent. The cabs replace autos. The weekend restaurant upgrades from ₹800 to ₹2,500. The "small treat" becomes ₹1,200 instead of ₹300.

The invisibility doesn't go away with more money. It just gets more expensive.

"I'll start tracking from next month"

No, you won't. Because next month will be "unusual" too. There will be a wedding. Or a festival. Or a work emergency. Or someone's birthday. Or your AC will break down.

There is no "normal" month. Every month has something.

The only way to know where your money goes is to look at this month, exactly as messy and unusual as it is.

"Tracking is for people who are struggling financially"

This is the most damaging myth.

Tracking isn't about poverty. It's about awareness. Some of the wealthiest families in India know exactly where their money goes — not because they're worried, but because clarity gives them power.

Not knowing where your money goes doesn't mean you're doing fine. It means you're flying blind.

How to Think About This Going Forward

Money flows to the path of least resistance

Your money doesn't go where you intend it to go. It goes where it's easiest to go.

Ordering food online is easier than cooking after a long day. Taking a cab is easier than waiting for an auto. Buying something on Amazon is easier than going to a store and comparing prices.

If you want to know where money is going, look for the friction-free paths.

The question isn't "Did I need this?"

That's a useless question because you can justify almost anything in the moment. You were tired. You were late. You were celebrating. You deserved it. It was on sale.

The better question is: "What pattern is this part of?"

One ₹600 Swiggy order isn't a problem. Twelve of them is a pattern. One ₹1,500 Saturday night out isn't a problem. Doing it every week is a pattern.

Patterns reveal behavior. Individual transactions don't.

Visibility comes before judgment

You can't fix what you can't see. And you shouldn't want to fix anything until you see it clearly.

The goal right now isn't to stop spending. It's not to feel guilty. It's not to become a person who tracks every ₹10 note.

The goal is to stop being confused about where your money actually goes.

Once you see the pattern — once you notice that food delivery is ₹8,000 a month, or that weekend spending is ₹6,000, or that "small cash withdrawals" are ₹5,000 — you can then decide what to do.

But deciding comes after seeing. Not before.

Your memory is a terrible accountant

You will not remember. This isn't a discipline problem. This is how human memory works.

We remember emotionally significant events. We forget routine ones. A ₹50,000 expense feels significant. A ₹300 expense 40 times does not.

If you rely on memory to know where your money went, you will always be surprised.

The invisible becomes visible only with a system

You don't need a complicated app. You don't need a color-coded spreadsheet. You don't need to account for every single rupee.

But you need something. A simple notes file. A basic expense app. Even just saving all payment screenshots in a folder for one month.

The system doesn't have to be perfect. It just has to exist.

Because the alternative is continuing to wonder, every month, where it all went.

Connecting the Dots

Where money goes is the foundation of everything else in your financial life.

If you don't know where it's going, you can't know how much you actually have to save. You can't set realistic goals. You can't make a plan. You can't figure out if you need to cut back, or if you're actually doing fine and just feeling guilty for no reason.

This isn't just about "tracking expenses." That's the mechanical part.

This is about developing financial visibility — the ability to see what's actually happening with your money, not what you think is happening or what you hope is happening.

Later, you'll learn to distinguish needs from wants. You'll learn to budget. You'll learn to allocate money toward goals. You'll learn to build surplus and invest it.

But all of that starts here. With one simple, uncomfortable question:

Where is my money actually going?

You'll encounter this question again and again, at every stage of financial maturity. Right now, it's about awareness. Later, it will be about optimization. Then about efficiency. Then about wealth-building.

But you can't skip this step. You can't optimize what you can't see.

The Real Shift

Money doesn't vanish. It never does.

It leaves. Through doors you opened without noticing. Through habits you formed without questioning. Through conveniences you chose without adding up the cost.

The reason most people don't know where their money goes isn't because they're careless or bad at math. It's because they're looking at individual trees and missing the forest.

One ₹300 expense is a tree. Fifteen of them is a forest.

This isn't about becoming paranoid or obsessive. It's about becoming awake.

When you actually see where your money goes — when you notice the patterns instead of just remembering the big transactions — something changes.

Not immediately. Not dramatically.

But you stop being confused. You stop feeling like money is something that happens to you.

And that clarity, by itself, is the beginning of control.

Smit Panchal

Chartered Accountant | Writing about Money, Clearly

Smit simplifies complex money concepts through first-principles thinking and real-world insights. Writing on personal finance, wealth frameworks, and financial clarity—beyond noise, products, and hype. Views expressed are personal and educational.

Connect on LinkedIn